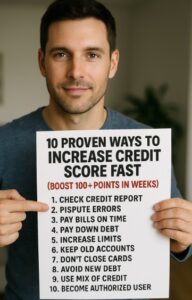

If you’ve recently been denied a loan, rejected for an apartment, or hit with high-interest rates, your credit score could be the silent deal-breaker. The good news? You’re not stuck with a bad score forever.

With the right tactics, you can increase your credit score fast—even within 30 days. Let’s break down how you can go from struggling to stellar credit, with proven, actionable strategies anyone can follow.

This guide is filled with practical steps, expert insights, and direct links to the best tools and resources. Whether you’re starting from scratch or recovering from financial setbacks, these strategies can get you closer to your financial goals quickly.

So let’s start fixing your credit score now. It’s easier than you think—and your future self will thank you for it. 🙌

🔎 Understanding Credit Scores

A credit score is a three-digit number that lenders use to determine your creditworthiness. It’s based on your credit report, which tracks how well you manage debt, including your payment history, amounts owed, credit age, new credit, and credit mix.

Most commonly, credit scores range from 300 to 850. A higher score means you’re more likely to get approved for loans and credit cards, and you’ll likely receive better terms like lower interest rates and higher credit limits.

FICO and VantageScore are the two major scoring models. They analyze your credit data slightly differently, but both place strong emphasis on your payment history and credit utilization.

👉 Credit Score vs Credit Report Explained – Know the difference before you start rebuilding.

📊 Credit Score Ranges Explained

| Score Range | Rating | What It Means |

|---|---|---|

| 300–579 | Poor | High risk to lenders |

| 580–669 | Fair | May get credit with higher rates |

| 670–739 | Good | Qualifies for most credit |

| 740–799 | Very Good | Low credit risk |

| 800–850 | Excellent | Best terms and rates |

Now that you know how the system works, let’s dive into the strategies that will get you to the “Excellent” range faster than you’d expect.

💸 Pay Down Credit Utilization Fast

Credit utilization refers to the percentage of your total credit limit you’re using. Keeping this below 30% is key—but for faster score boosts, aim for under 10%.

One of the fastest ways to increase your credit score is to pay off high balances—especially if you can bring any revolving debt to under 10% of the limit. This change can reflect within days after your creditors report to bureaus.

Example: If your credit card limit is $5,000, keeping your balance below $500 can give your score a healthy bump. It’s one of the top insider hacks for score increases in under 30 days.

👉 Credit Utilization Ratio Tips You Must Know

📈 Fast Impact Strategies for Utilization

| Tip | Action | Result |

|---|---|---|

| Pay twice a month | Reduce balance before statement date | Prevents high utilization reporting |

| Ask for credit limit increase | Contact issuer after on-time payments | Boosts available credit instantly |

| Use multiple cards | Spread charges across accounts | Keeps each card’s usage low |

💳 Use the Right Credit Cards

If you’re just starting to build or rebuild your credit, secured credit cards are a solid tool. They work like regular cards but require a refundable deposit, which acts as your credit limit.

Using a secured card responsibly—making small purchases and paying in full every month—can rapidly increase your score. Some issuers even upgrade you to an unsecured card after consistent use.

Many people overlook this, but getting added as an authorized user on a trusted person’s card can also help you gain positive payment history without applying for a new line of credit.

👉 Best Secured Credit Cards for 2025 – Start with cards that report to all three bureaus.

📌 Top Benefits of Secured Credit Cards

| Feature | How It Helps Your Score | Extra Perk |

|---|---|---|

| Monthly reporting | Builds payment history | Improves score fast |

| Low deposit options | Accessible for most people | Start as low as $49 |

| Graduation to unsecured | Increases credit mix | Refunds your deposit |

🏠 Loan Approval & Credit Score

Your credit score plays a huge role in whether you’re approved for personal loans or mortgages. Lenders look for consistency, low debt, and responsible repayment behavior.

For mortgages, a FICO score of at least 620 is typically required for conventional loans. FHA loans may accept scores as low as 580, but with stricter conditions or higher down payments.

Personal loans usually require a score of 600+, but the better your score, the lower your interest rate will be. Every 20-point increase can save you hundreds or even thousands in interest over time.

👉 Minimum Credit Score for Mortgage Approval – Know where you stand before you apply.

🏡 Mortgage vs Personal Loan Requirements

| Loan Type | Minimum Score | Best Terms at |

|---|---|---|

| Conventional Mortgage | 620 | 740+ |

| FHA Mortgage | 580 | 680+ |

| Personal Loan | 600 | 720+ |

📱 Best Apps for Monitoring Credit

You can’t improve what you don’t track. That’s why credit monitoring apps are essential tools for boosting your credit score fast. They alert you to changes, help spot errors, and keep you motivated.

Apps like Credit Karma, Experian Boost, and myFICO provide free access to your score, breakdowns of each factor, and alerts when new accounts or inquiries appear.

I’ve found that seeing score movement weekly gave me the push I needed to keep paying down debt and using my cards wisely. It’s almost like a credit fitness tracker!

👉 Top Credit Score Monitoring Apps – Stay informed and in control.

📱 Top Credit Monitoring Apps Compared

| App | Free? | Key Feature |

|---|---|---|

| Credit Karma | Yes | VantageScore + account alerts |

| Experian Boost | Yes | Adds utilities & Netflix to report |

| myFICO | No | True FICO score + full reports |

📅 Fix Late Payments Strategically

Late payments can tank your credit score—sometimes by over 100 points. The later the payment and the more recent, the worse the damage. But there are ways to minimize the impact.

Start by bringing all accounts current. Then, reach out to your creditors and request a goodwill adjustment—especially if you’ve been a solid customer and the late payment was a one-time mistake.

You can also dispute inaccurate late payments with the credit bureaus. If the creditor can’t verify it, they’re required to remove it from your report under the Fair Credit Reporting Act.

👉 How Late Payments Affect Credit Score – And what you can do to fix them.

🧹 Methods to Remove Late Payments

| Method | Description | Effectiveness |

|---|---|---|

| Goodwill Letter | Ask lender to remove late mark | High (if history is good) |

| Dispute with Bureau | Challenge the accuracy | Medium |

| Pay for Delete (rare) | Negotiate removal with payment | Low (not always allowed) |

FAQ

Q1. How fast can I improve my credit score?

A1. With strategic actions like lowering utilization and disputing errors, some people see a 50–100 point increase in as little as 30 days.

Q2. What’s the best way to start building credit from scratch?

A2. Start with a secured credit card or become an authorized user on a family member’s card that has a good history.

Q3. Will checking my score lower it?

A3. No! Soft inquiries, like checking your own score with apps, have zero impact on your credit.

Q4. Can I get a mortgage with bad credit?

A4. Yes, but terms will be less favorable. FHA loans are more flexible but usually require 580+ credit scores.

Q5. How many credit cards should I have?

A5. There’s no perfect number, but 2–3 responsibly used cards can help build a strong credit mix.

Q6. What is credit utilization again?

A6. It’s the percentage of your total available credit that you’re using. Aim to keep it below 30%, or under 10% for faster results.

Q7. What hurts my credit score the most?

A7. Late payments, maxed-out credit cards, and collections accounts are the most damaging factors.

Q8. Can I fix my credit on my own?

A8. Absolutely! With the right steps and consistency, you can improve your credit without paying for expensive services.

Disclaimer: The information provided in this blog is for educational purposes only and should not be considered financial or legal advice. Always consult a licensed financial advisor or credit expert before making decisions based on your credit.